Mortgage delinquencies and climate risk

The tail risks of agency credit risk transfer pools

Published

May 2024

After extreme weather events and natural disasters in the United States, there is often a rise in mortgage delinquencies as people struggle with loss of income and repair costs. Extreme heat, wildfires, and hurricanes have all been linked to increased rates1,2,3 though the size of the effect varies. Past research conducted by risQ, which was subsequently acquired by ICE in 2021, also suggested that physical climate risk is associated with higher rates of delinquency even after accounting for macroeconomic factors, local socioeconomic factors, and loan attributes.4 For homeowners in highly exposed areas, these trends are worrying. Homes in high-risk areas have lower rates of price appreciation than homes in low-risk areas;5 as insurance rates continue to increase in many parts of the country,6 some homeowners may even find their houses losing value.

These trends also have broader ramifications for American taxpayers. In the aftermath of large natural disasters, there is evidence that lenders preferentially approve loans that can be securitized and transferred off the lenders’ balance sheets. The effects can be substantial: one study found that probabilities of securitization increased by more than 19% after large climate-related events, and the differences in approval rates for conforming and jumbo loans increased by more than 7%.7 At the time of the study’s publication, The New York Times published an article entitled “Climate Risk in the Housing Market has echoes of Subprime Crisis, Study says,” referencing the climate risks that are implicitly shouldered by the government sponsored enterprises and the Federal Government.8

For private investors, these patterns of risk transfer may have the most immediate implications for Credit Risk Transfer (CRT) pools. Both Fannie Mae and Freddie Mac started Credit Risk Transfer Programs in 2013 with the goal of transferring some of their overall risk to private investors. Annual CRT issuance is substantial: In 2021, the reference pools for Fannie and Freddie’s total CRT issuance represented $1.1 trillion in unpaid principal balance.9 In contrast to government-sponsored enterprise pools and Real Estate Mortgage Investment Conduits (REMICs), investors in CRTs take on credit risk.

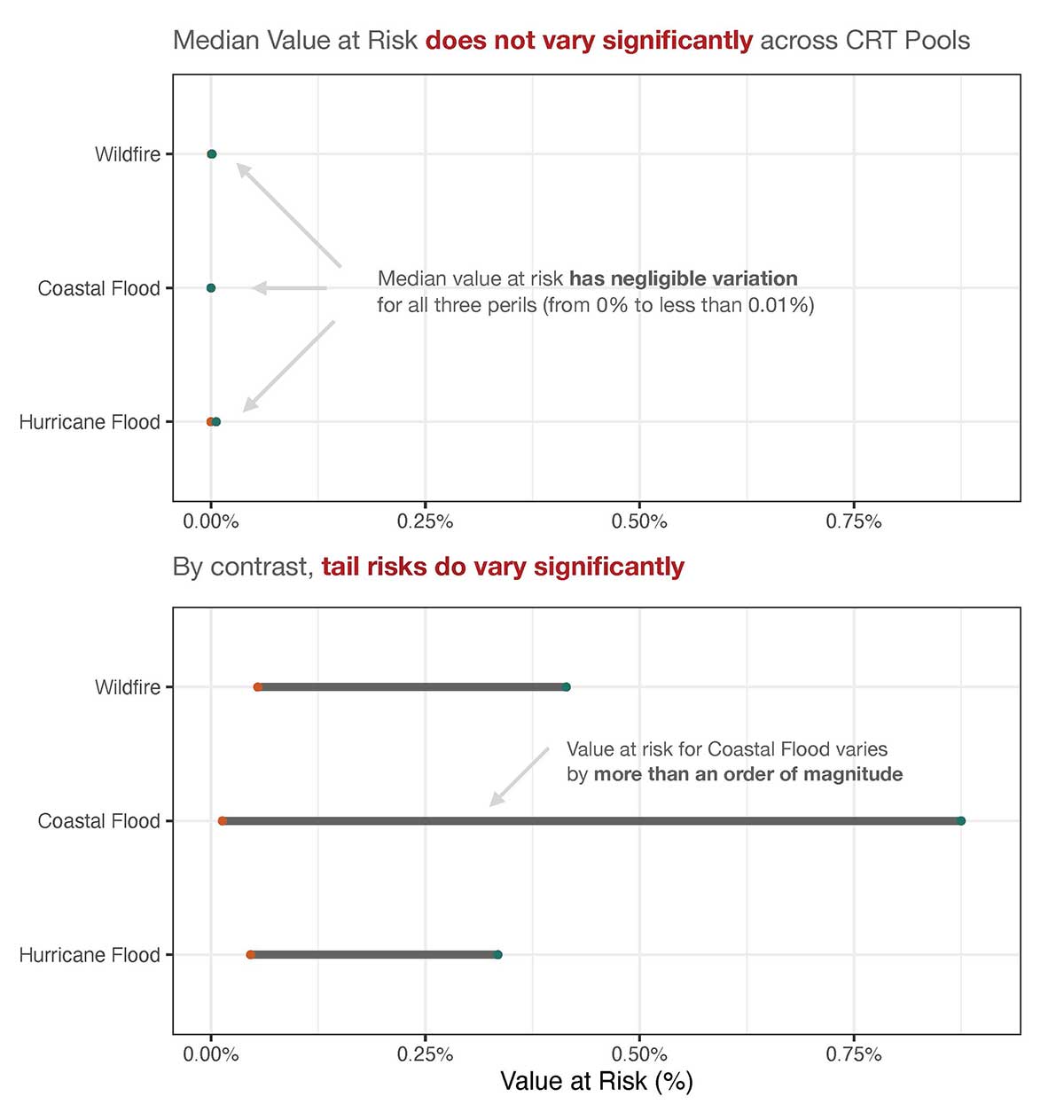

‘Value at risk’ is a common framework within the insurance industry that attempts to capture the degree of possible losses of an asset over a given time frame. ICE Sustainable Finance’s value at risk projections for CRT pools represent expected annual losses as a percentage of the replacement costs of homes securing loans in each pool.

Based on a factor date of November 1, 2023, ICE Sustainable Finance’s assessments of the current median value at risk because of coastal flood and wildfire risks are negligible across all pools (Figure 1, top). For hurricane flooding, the median property value at risk varies from 0% to only 0.006%10 These pools can contain thousands of mortgages with geographically distributed collateral. It makes sense that given such large and diverse samples, the median climate risk of each pool would be similarly small.

FIGURE 1. (top) The range of values of the median property value at risk associated with each of the climate metrics across dozens of CRT pools. (bottom) The range of values of the 95th percentile of property value at risk associated with the same climate metrics. For coastal flooding in particular, the physical risk exposure of the most exposed properties – “the riskiness of the riskiest” – in different CRT reference pools varies by an order of magnitude.

(Source: ICE Sustainable Finance as of 3/25/24)

However, median risks across reference pools do not tell the full story, because CRT pools do vary significantly in terms of the risk of the most exposed pool collateral. Coastal flood risk is a particularly dramatic example. In some CRT pools, the estimated value at risk of the 5% riskiest properties for coastal flooding is greater than 0.01%, while in other pools, it is larger than 0.87% – a difference of over an order of magnitude (Figure 1). Significant variations in tail risks also exist, though not to such an extreme degree, for perils like wildfire and hurricane flood. Although these value-at-risk percentages may seem small in absolute number, they are material because of the structure of CRT instruments. Investors in the riskiest tranches of these pools could lose money even if just a small proportion of collateral in the reference pool defaults.

Going forward, ICE’s new relationship with leading mortgage analytics firm DeltaTerra Capital will help to illuminate the potential impacts of these sorts of physical climate risks on mortgage markets. The collaboration will enable both firms to translate climate model projections and insurance market data into actionable risk metrics for financial market stakeholders, including asset price depreciation risk and pool loss projections for different economic and climate scenarios.

1 Deng, Y, CHan, T Li & T Riddiough (2021). Whither Weather?: High Temperature, Climate Change and Mortgage Default. Paris December 2021 Finance Meeting EUROFIDAI – ESSEC. Link

2 Biswas, S, Hossain, M, & D Zink (2023). California Wildfires, Property Damage, and Mortgage Repayment. Federal Reserve Bank of Philadelpha. Working Paper WP23-05. Link

3 Du, D, & X Zhao (2020). Hurricanes and Residential Mortgage Loan Performance. Officer of the Comptroller of the Currency Report. Link

4 risQ, Inc. (7 Jul 2021). Climate Risk is Already Impacting US Fixed Income Fundamentals, Medium Blog Post. Link

5 risQ, Inc. (7 Jul 2021). Climate Risk is Already Impacting US Fixed Income Fundamentals, Medium Blog Post. Link

6 Allen, G. (26 Oct 2023) Feeling the pinch of high home insurance rates? It’s not getting better anytime soon. NPR News. Link

7 Ouazad, A & M Kahn (2019). Mortgage Finance and Climate Change: Securitization Dynamics in the Aftermath of Natural Disasters. NBER Working Paper No. 26322. Link

8 Flavelle, C. (27 Sep 2019). Climate Risk in the Housing Market Has Echoes of Subprime Crisis, Study Says. The New York Times. Link

9 Credit Risk Transfer Progress Report (Fourth Quarter 2021). Federal Housing Finance Agency. Link

10 Unless stated otherwise, all numbers and statistics are based on ICE Sustainable Finance data as of 11/15/2023.